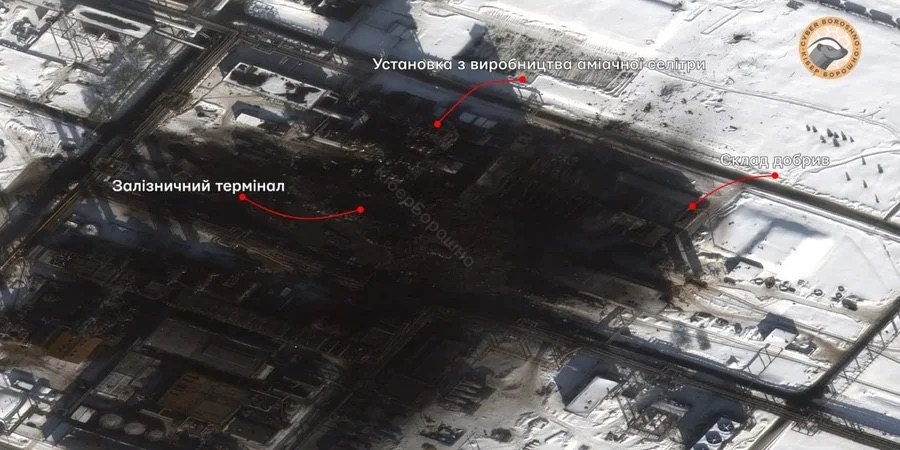

In February, Ukraine’s Defence Forces struck the Dorogobuzh plant: seven people were killed, the railway station was effectively wiped out, and around 5% of Russia’s ammonium nitrate output was taken offline (with operations not expected to resume before May). On 19 March, Nevinnomyssk Azot (part of EuroChem) was hit — a drone strike on one of the world’s largest plants, knocking out its acetic acid production unit. Then, on 13 April, Cherepovets Azot (PhosAgro) was targeted — a major strike. Drones from Ukraine’s Unmanned Systems Forces reached the industrial giant in the Vologda region. Two out of three units of the nitrogen complex were damaged, and Cherepovets produces hundreds of thousands of tonnes of ammonia and ammonium nitrate annually.

The market is reacting. On Europe’s Freedom Finance platform, for example, fully protected investments in grain have appeared amid concerns over the Strait of Hormuz and fertiliser shortages. Several major wars are consuming explosive precursors, with Ukraine and Russia absorbing them at scale. Iran has been affected by strikes on chemical plants, fuel prices are rising, and spare parts have become less accessible due to disrupted logistics and the prioritisation of military production — all expected consequences. Russia has imposed a ban on ammonium nitrate exports until the end of April — a clear warning sign. A ban on industrial sulphur exports has also been extended until June 2026, affecting a key input for fertiliser production.

This suggests that strikes should not focus solely on oil refineries, transhipment hubs and gas infrastructure. The chemical industry is an ideal target: its effects ripple across agriculture, light industry and processing — ultimately reducing the financial resources available for the war.

Why are our strikes intensifying? First, there is a need to slow down the production of glide bombs (KABs) and artillery shells, and ammonium nitrate is a key precursor. Moscow plans to produce around four million shells and mines in 2026 — a figure that is clearly unacceptable from Ukraine’s perspective. That is why the effort targets the entire production chain: from shell manufacturing and heat treatment to fuses.

Second, Europe is on the verge of a major scaling-up of cruise missile and UAV production. And not just FPV drones or reconnaissance wings, but systems with medium and long range. France’s Chorus project, along with AASM Hammer glide bombs (up to 100 per month), is expanding output, while production of the Ruta missile is being localised at Rheinmetall facilities. The momentum is building. In 2026, joint ventures have become operational, including with companies such as Fire Point. In Denmark, Ukrainian FP-5 Flamingo drones are being assembled and solid fuel is produced for them, while Germany manufactures the airframes.

Europe’s leading missile manufacturer, MBDA, reached peak capacity in 2026, increasing production of Storm Shadow and SCALP-EG missiles by 40% in just one year. An upgraded Mk2 version is now entering serial production. It features a completely redesigned guidance system, making it resistant to even the most advanced electronic warfare systems, as it relies not only on terrain and digital mapping but also on imagery of the target itself. MBDA has also launched a ground-based version of its naval cruise missiles (LCM), removing the need to deploy them from aircraft such as the Su-24 and preserving valuable airframe resources. They can now be launched from standard truck-mounted systems — meaning even more strikes against industrial facilities deep inside Russia.

The EU has moved away from supplying a patchwork of different equipment. The focus now is on standardisation: three or four core models around which factories and production lines are being organised. The Soviet Union once relied on mass production of the T-34 — a tank that was, on average, inferior to many specialised German machines. The Red Army lost close to 90,000 of them, yet the emphasis on scale ultimately proved decisive. Now, the aim is to introduce Moscow to its own preferred formula — mass Western production.

Most new Western systems are equipped with automatic target acquisition (machine vision). This reduces Russia’s advantage in electronic warfare and forces it to spend more on interceptors. And interceptors cannot, for example, be used to support assaults on the ground. Diverting resources away from expanding production of infantry fighting vehicles and armoured personnel carriers, while forcing losses in costly frontal assaults using motorcycles and quad bikes, becomes strategically valuable. Localisation is also playing a role: some components — such as airframes and warheads — are produced in Ukraine, while guidance systems and engines come from the EU. This helps bypass bureaucratic constraints and, for now, makes it difficult for Russia to strike European production facilities with systems such as Iskander missiles.

Thirdly, there is the recent development that Germany will produce 3,000 GEM-T missiles for Patriot systems at its own facilities and expense for Ukraine and the EU. While deliveries are expected in 2027–2028, these are effectively state-backed guarantees. With funding secured, existing stockpiles can be transferred earlier, with around 750 missiles planned for 2026–2027. Although they are not capable of intercepting Kinzhal missiles, they are effective against ballistic threats such as Iskander. This means greater security for deploying new industrial facilities in Ukraine and enables additional transfers from EU reserves.

Fourthly, if this is combined with the satellite constellation that the EU is deploying specifically for targeting (the IRIS² project), Moscow will soon have no safe zones left, even beyond the Urals. With high-quality imagery of targets, knowledge of radar activation schedules, and airborne early warning radar coverage extending hundreds of kilometres via rotating sorties, it becomes possible to plan near-optimal strike routes.

As for finances: Russia remains consistently among the world’s top three exporters of fertilisers. In 2025, it earned around $16–18 billion from this sector. Despite sanctions, the EU still sources roughly 16% of its fertiliser imports from Russia (although this share is declining). This is hard currency that Russia uses to procure chips via third countries and pay contract soldiers.

Agricultural exports bring in even more. In 2025, they reached a record $41.5 billion, with grain accounting for around $18–20 billion. Despite strikes on ports, Russian grain exports increased by 52% at the start of 2026 compared to the previous year. Russia is using aggressive undercutting to push competitors out of the market and secure fast cash flow to sustain the war in the short term.

Read alsoRussian plans and the mathematics of death

Official Rosstat data for March is still being compiled, but according to preliminary estimates and Russian Railways (RZD) data, growth in fertiliser production has slowed to zero or turned negative. Fertiliser shipments by rail in the North-Western region fell by 2.5% in the first quarter, while transshipment in Baltic ports dropped by 12% in the first two months of 2026. The reasons cited are a shortage of vessels and systemic disruptions in port operations. Together with export restrictions, this is a typical sign that strikes are having an impact — and a significant one. The agricultural sector sustains the wider economy, but when there is no ammonium nitrate to feed both fields and artillery at the same time, a choice must be made. The Kremlin has chosen artillery, which means the agricultural sector is likely to come under pressure as well.